Is a Home Equity Line of Credit right for you?

Share this article

Owning a home comes with many benefits. Aside from pride of home ownership and an ability to personalize your living space, homes also typically increase in value which allows you to build equity (the difference between the market value of your home and the money you owe on it). If you build up enough equity, you can consider accessing for whatever you need, such as home renovations, investments, or paying off high-interest debts. Interested? Allow us to introduce you to a product that can be used to make the most of the money you already have: CUA's Home Equity Line of Credit, or HELOC.

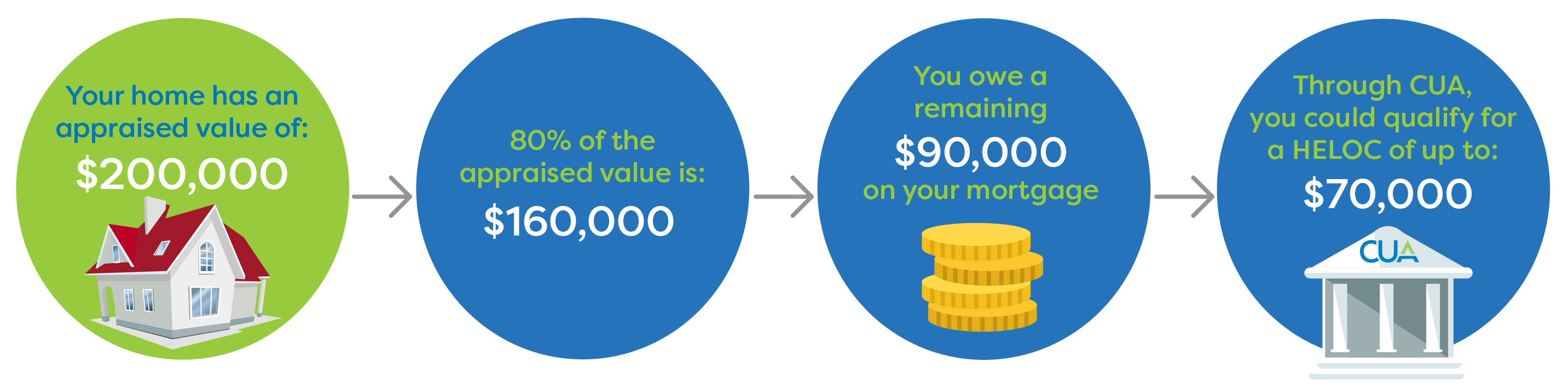

CUA's HELOC can provide you with up to 80% of the appraised value of your home, less the outstanding balance of your mortgage. This is a significant benefit in that the chartered banks are limited to lending home equity at a maximum of 65% of your home’s appraised value. You can also enjoy these funds at a much lower interest rate than using higher interest rate products, such as credit cards or loans. Let's look at this example together:

Let's say, of the $70,000 you've qualified for, you wish to use $20,000 for a kitchen renovation or for energy-efficient upgrades, such as new appliances or windows. The $20,000 can be set for a monthly repayment of interest-only or at a fixed monthly amount - it's your choice! It's important to note that the monthly interest payment on the HELOC must be made in addition to your monthly mortgage payment.

When used responsibly and with a long-term repayment plan in place, a HELOC can be a wonderful financial tool to make use of for various aspects of your life. It's important, however, to make sure that the debt you take on is both necessary and affordable. I recommend always keeping a tab on the total balance of your HELOC, particularly if you plan to sell your home in the near future. By paying down your HELOC before you sell your home, you can ensure you don't end up responsible for a large HELOC repayment afterwards. And like all other lending products, HELOCs are subject to approval criteria, such as a credit check.

If you think a HELOC may be a perfect solution for your current or future needs, I would be happy to meet with you to discuss this option further. Contact us at info@cua.com or 902.492.6500 to schedule a personalized meeting.

Revised Jul. 4, 2021

CUA's HELOC can provide you with up to 80% of the appraised value of your home, less the outstanding balance of your mortgage. This is a significant benefit in that the chartered banks are limited to lending home equity at a maximum of 65% of your home’s appraised value. You can also enjoy these funds at a much lower interest rate than using higher interest rate products, such as credit cards or loans. Let's look at this example together:

Let's say, of the $70,000 you've qualified for, you wish to use $20,000 for a kitchen renovation or for energy-efficient upgrades, such as new appliances or windows. The $20,000 can be set for a monthly repayment of interest-only or at a fixed monthly amount - it's your choice! It's important to note that the monthly interest payment on the HELOC must be made in addition to your monthly mortgage payment.

When used responsibly and with a long-term repayment plan in place, a HELOC can be a wonderful financial tool to make use of for various aspects of your life. It's important, however, to make sure that the debt you take on is both necessary and affordable. I recommend always keeping a tab on the total balance of your HELOC, particularly if you plan to sell your home in the near future. By paying down your HELOC before you sell your home, you can ensure you don't end up responsible for a large HELOC repayment afterwards. And like all other lending products, HELOCs are subject to approval criteria, such as a credit check.

If you think a HELOC may be a perfect solution for your current or future needs, I would be happy to meet with you to discuss this option further. Contact us at info@cua.com or 902.492.6500 to schedule a personalized meeting.

Revised Jul. 4, 2021

Read More

|

|

|